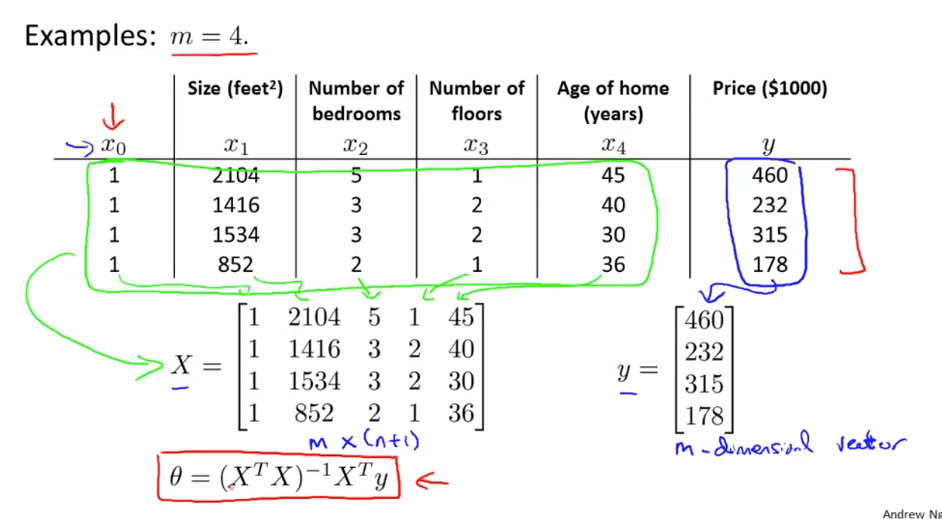

Normal Equation in Linear Regression

Detailed explanation of the Normal Equation for linear regression, including matrix formulation, closed-form solution, comparison with gradient descent, and practical considerations for implementation.

Normal Equation (Closed-Form Solution)

Instead of solving multiple iteration of gradient descent, Normal equation can get theta in one step

- Θ can be directly calculated where cost function is minimal using calculus in one step instead of iterating iterative optimization:

Advantages

- No learning rate required

- Direct computation

Limitations

- Computationally expensive for very large datasets

- Matrix inversion can be costly

Steps:

- Construct design matrix X using feature columns and add 1 in first column

- Construct y vector using result values Y

- calculate:

Θ = (XTX)-1 XTy

Feature scaling is not required for Normal Equation method

Normal Equation vs Gradient Descent:

| Feature | Gradient Descent | Normal Equation |

|---|---|---|

| Complexity | Complex need to debug alpha | Convenient & Simple to implement |

| Choose Learning Rate(α) | Required | No need |

| Feature Scaling | Required | No need |

| Iteration | Many Iteration Required | Not required |

| Feature Set>=million | Efficient if n is huge O(kn2) | Slow if n is huge, cost of inverse matrix is O(n3) |

| Complex Learning Algo | Can used for Complex learning algo | Not supported |

Inverse Matrix(A-1)

A' called inverse if

A'.A = A'.A = I

Matrix without Inverse called Degenerate Matrix/ Singular/ Non Invertible

Cause for non invertible Matrix:

- Redundant feature: two feature related by a linear equation x2 = kx1 eg: size in feet and meter

- More feature than training set(m<=n)): delete some feature or use regularization

Octave method for inverting matrix:

- pinv(A) : Pseudo Inverse, calculates inverse even if matrix is non invertible

- inv(A) : Inverse