Normal Equation in Linear Regression: Formula, Intuition, and Comparison with Gradient Descent

Understand the Normal Equation in linear regression, its closed-form solution, mathematical formula, advantages, limitations, and how it compares to gradient descent for model optimization.

Cost Function Regularization: Balancing Bias and Variance in Machine Learning Models

Support Vector Machines (SVM): Maximizing Margins for Robust Machine Learning Models

Normal Equation (Closed-Form Solution)

Instead of solving multiple iteration of gradient descent, Normal equation can get theta in one step

- Θ can be directly calculated where cost function is minimal using calculus in one step instead of iterating iterative optimization:

Advantages

- No learning rate required

- Direct computation

Limitations

- Computationally expensive for very large datasets

- Matrix inversion can be costly

Steps:

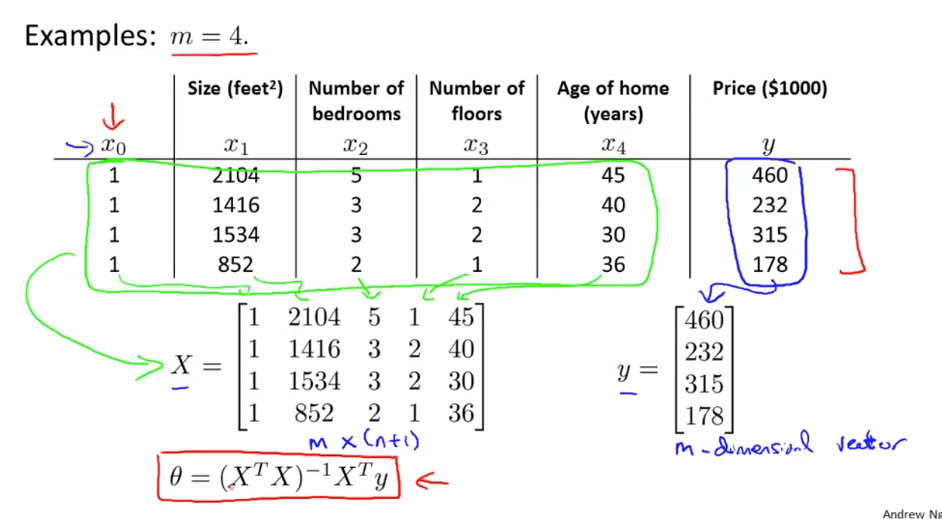

- Construct design matrix X using feature columns and add 1 in first column

- Construct y vector using result values Y

- calculate:

Θ = (XTX)-1 XTy

Feature scaling is not required for Normal Equation method

Normal Equation vs Gradient Descent:

| Feature | Gradient Descent | Normal Equation |

|---|---|---|

| Complexity | Complex need to debug alpha | Convenient & Simple to implement |

| Choose Learning Rate(α) | Required | No need |

| Feature Scaling | Required | No need |

| Iteration | Many Iteration Required | Not required |

| Feature Set>=million | Efficient if n is huge O(kn2) | Slow if n is huge, cost of inverse matrix is O(n3) |

| Complex Learning Algo | Can used for Complex learning algo | Not supported |

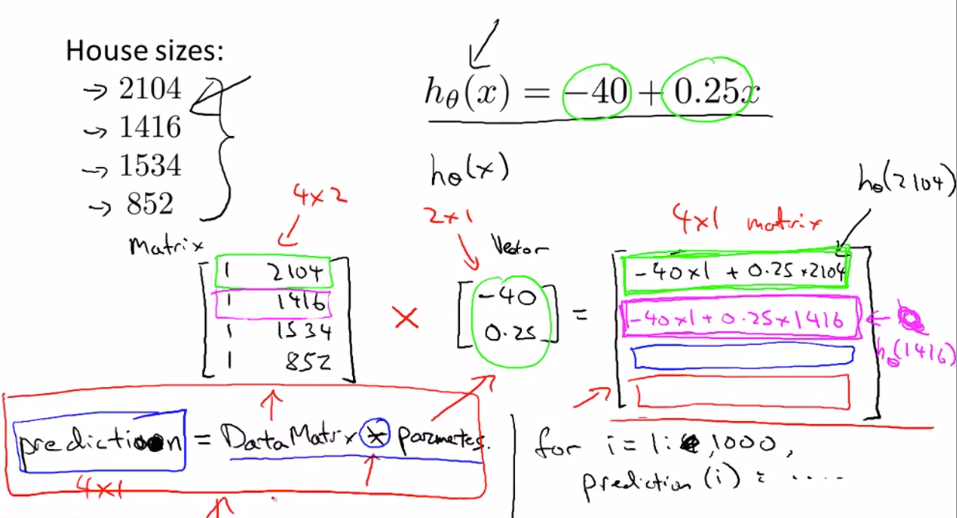

Faster single Hypothesis Prediction calculation given data set and Thetas **Much faster than nested for loops

Data Matrix * Parameter Vector = Prediction Vector

h(x) = Theta0 + Theta1x

[1 , x]*[Theta Vector] = [h(x)]

Usage:

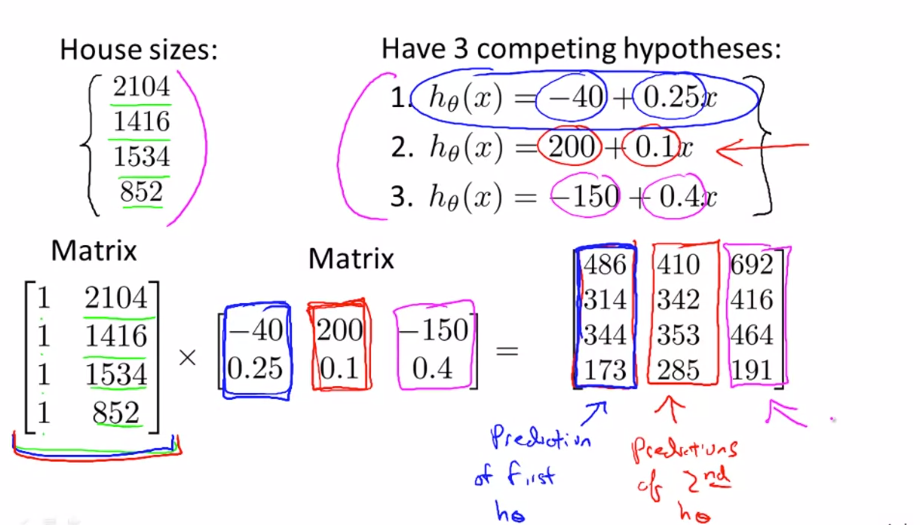

- Faster multiple Hypothesis Prediction calculation given data set and Thetas

- Much-much faster than nested for loops

Data Matrix * Parameter Matrix = Prediction Matrix

given h(x) = Theta0 + Theta1x

[1 , x]*[Theta Matrix] = [h(x)]

Normal Equation with Regularization

Instead of iterative gradient descent, we can use the normal equation.

Without Regularization:

With Regularization (Ridge Regression):

This discourages large parameter values and reduces overfitting.

Where Matrix

Properties:

- It is almost the identity matrix except the top-left element is 0.

- Dimension:

First diagonal entry is 0 because no regularization for

Remaining diagonal entries are 1 because we regularize to .

This ensures:

- (bias term) is not regularized

- All other parameters are regularized

Why Regularization Helps

If , then is non-invertible.

If , it may or may not be invertible.

where

- = number of training examples

- = number of features

In other terms if , then:

is non-invertible.

However, with regularization we add to :

That makes whole term invertible (for ).

This improves numerical stability.